Understanding Credit Scores: What Are They, Why They Matter

We all have them. In fact, most of us have more than one, and nearly everything we do affects them. Whether you use your credit card at the checkout counter, or get a no-interest loan for new furniture, your credit score is a record of your spending habits.

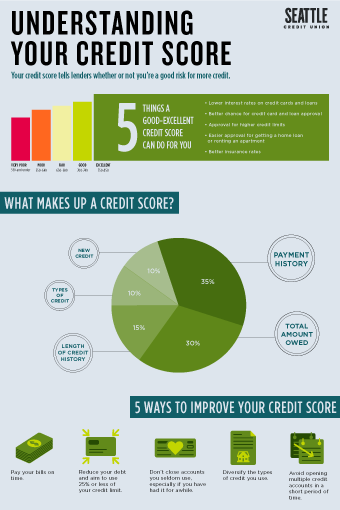

The three-digit numbers of your credit score ultimately tell lenders whether or not you’re a good risk for more credit, whether it’s a mortgage, a car loan, or a credit card. The higher your number—somewhere between 300 and 830—the more trustworthy you appear to potential lenders. But credit scoring isn’t foolproof.

How it works

There’s a huge variation in scoring models, but most are based on information compiled by the three big reporting agencies: Experian, Equifax, and TransUnion. Credit reports are made up of your credit history, which includes the types of credit you have, how much credit you have access to, how much of that you’ve borrowed, how long you’ve held your accounts, and if you pay your debts on time.

But how your score is assessed isn’t quite that simple.

Each of these three agencies can assign their own credit score. These are often called “educational scores” because they educate consumers about their credit status, using the agency’s own proprietary model. Yet most lenders use a scoring method that comes through the Fair Isaac Corporation, or FICO. FICO uses as least 60 different scoring models, many based around the type of loan you’re seeking.

What’s more, while the big three compile your historical records, the score they assign is based on what lenders have reported about their credit experience with you—and lenders don’t necessarily report to all three. Your lender may also use a different scoring model based on the types of loans they offer and what they deem important to know about you.

The big three agencies saw a need for more consistency and developed VantageScore, a scoring model that boasts greater accuracy and better matching of people to financial products. Some of the larger banks that offer your credit score for free using their services or mobile apps use VantageScore.

Regardless of which is scoring model is used, there may still be some variation due to the information each agency has about your spending. But the variation shouldn’t be too great.

What’s in a credit score?

Also factored in to your credit score, in addition to the credit spending your lenders report to the agencies, is the number of hard inquiries you’ve had about your credit. Too many may be a red flag for lenders, suggesting you’re having financial challenges if you’re seeking more credit, or that you’re not using credit wisely. What’s a hard inquiry? Any application submitted for the following:

- Mortgage

- Auto loan

- Credit card

- Student loan

- Personal loan

- Apartment rental

Soft inquiries usually won’t affect your credit score. These inquiries include checking your scores, pre-qualified credit card offers you didn’t ask for, pre-qualified insurance quotes, employment verification and background checks. Note, though, that utility, internet and cellphone providers may check your credit and these could be considered a hard inquiry. It’s a good idea to ask.

If you check your credit report and see a hard inquiry you didn’t ask for, you can dispute it with the credit bureau or the Consumer Financial Protection Bureau. It’s a good idea, as a hard inquiry could be an indicator of fraud.

None of your personal information is factored into a credit report or score – information like marital status, employment status, or even gender.

Smart credit

Your credit score contributes to the rates and fees you’ll pay to a lender; those with higher credit scores typically pay fewer fees and lower rates.

Whether or not you’re considering a loan, it’s a good idea to keep an eye on your credit score. At least once a year, take a good look at your report. You’re eligible for a free credit report from each of the three reporting agencies once per year, which means you can check your report three times a year.

The bottom line? Keep your credit scores high with these few tips:

- Pay bills on time

- Keep credit card use to no more than 30% of the total credit available. This number may vary depending on credit bureaus.

- Maintain a track record by having older credit accounts

- Have a mix of credit types, e.g., mortgage, Visa or MasterCard, store card, or car loan

TransUnion's path to improve your FICO recommendations:

- Age of your oldest account

- Less than 2 years is below average

- 2-7 years is average

- 8-25 years is good

- More than 25 years is excellent

- Percent of credit used

- Inquiries made in the past 2 years

- More than 5 years is below average

- 3-5 years is average

- 1-2 years is good

- None is excellent

- Accounts opened in the past 2 years:

- More than 6 years is below average

- 5-6 years is average

- 3-4 years is good

- Less than 3 years is excellent

If you feel you’ll benefit from debt counseling, or want to learn more about money management and potentially increase your credit score, you can find resources at Aquila Standard resources.

Download our infographic breaking down various factors that influence your credit score.